Seung Heo and Merih Uctum

February 25, 2026

This article summarizes major characteristics of the US economy in 2025, the challenges and opportunities it faces ahead.

I. The Real Economy

The US economic activity is growing steadily. Current GDP is growing above the potential GDP that would have prevailed had the last two crises not occurred.

A strong post-pandemic recovery is tapering off. Compared to previous business cycles, the economy emerged from the last recession vigorously, but its momentum is decelerating relative to the earlier recoveries.

The slowdown is reflected in both consumption and investment. We observe a K-shaped growth pattern, which describes an economy where different groups recover and grow at markedly different rates after a downturn. As in the letter “K”, the upper arm rises sharply (wealthy individuals, tech/asset-heavy sectors booming) while the lower arm declines or stagnates (lower-income earners, struggling industries). This divergence allows the wealthy to accumulate further gains through investments, such as stocks and real estate, while many others face stagnant wages, inflation, and financial strain, leading to increased inequality.

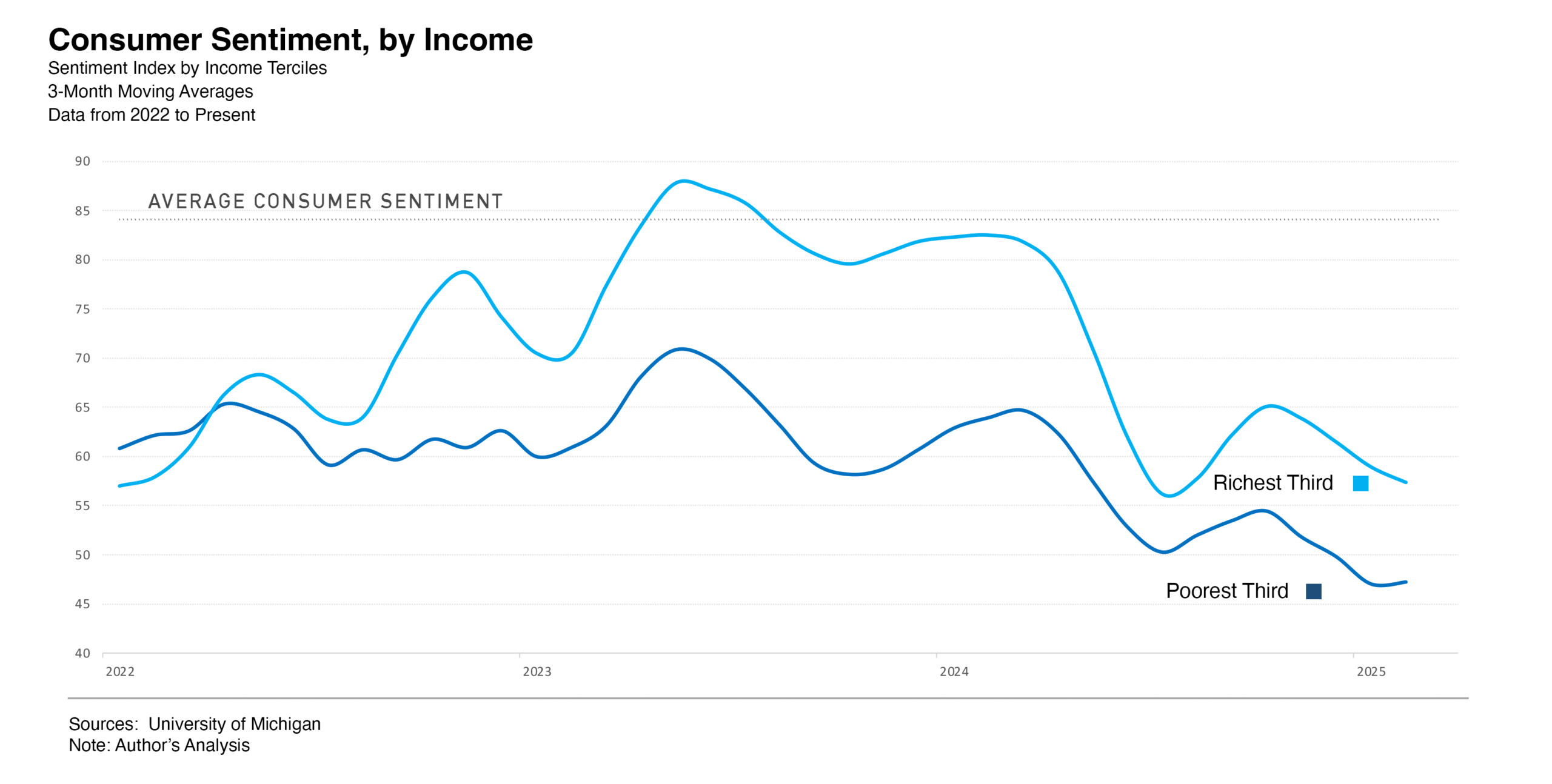

When considering consumption, there is historically low consumer sentiment, revealing a K-shaped recovery in sentiment. Even though total consumption is holding steady. Consumer sentiment reached historic lows in all income categories.

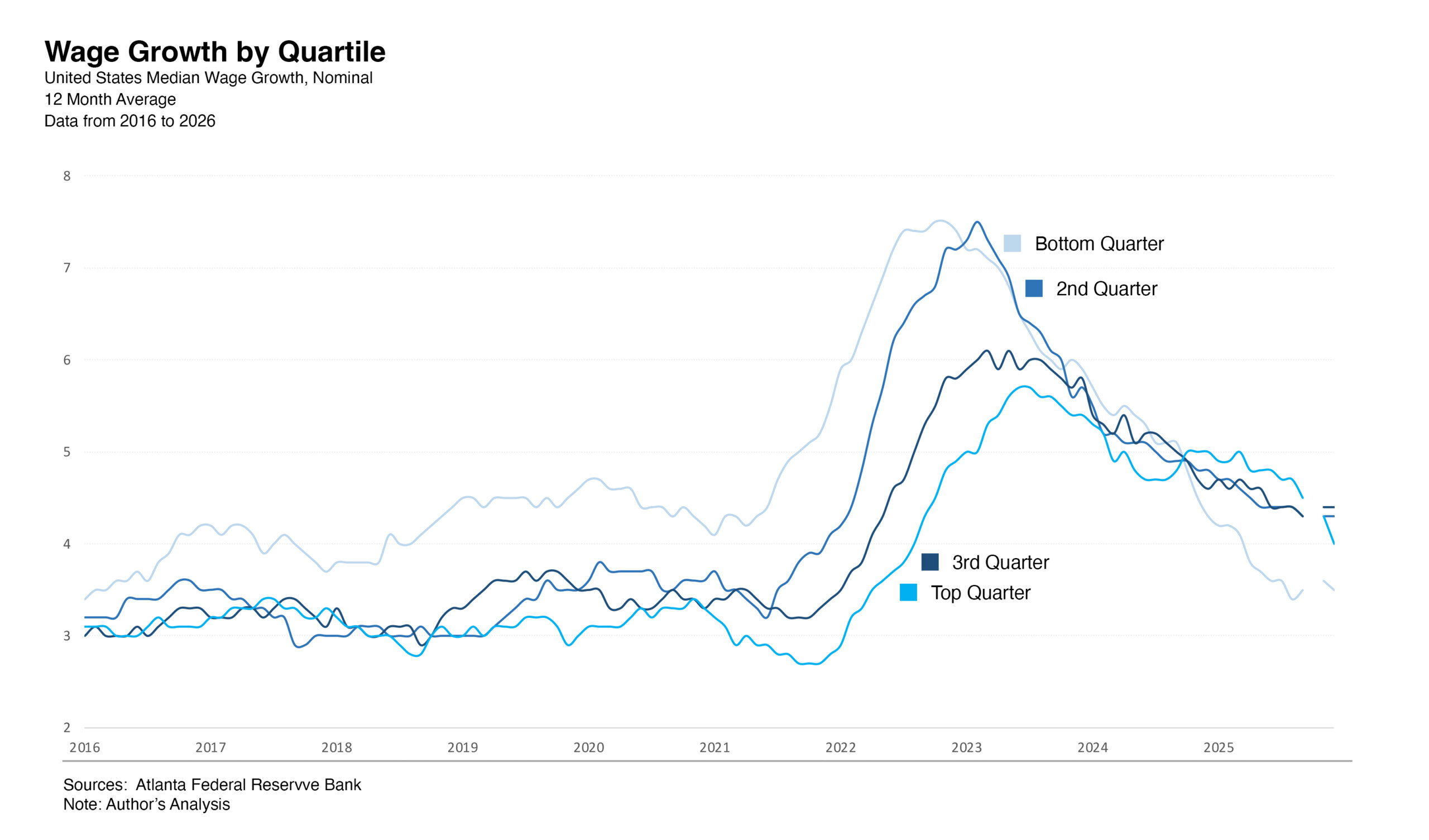

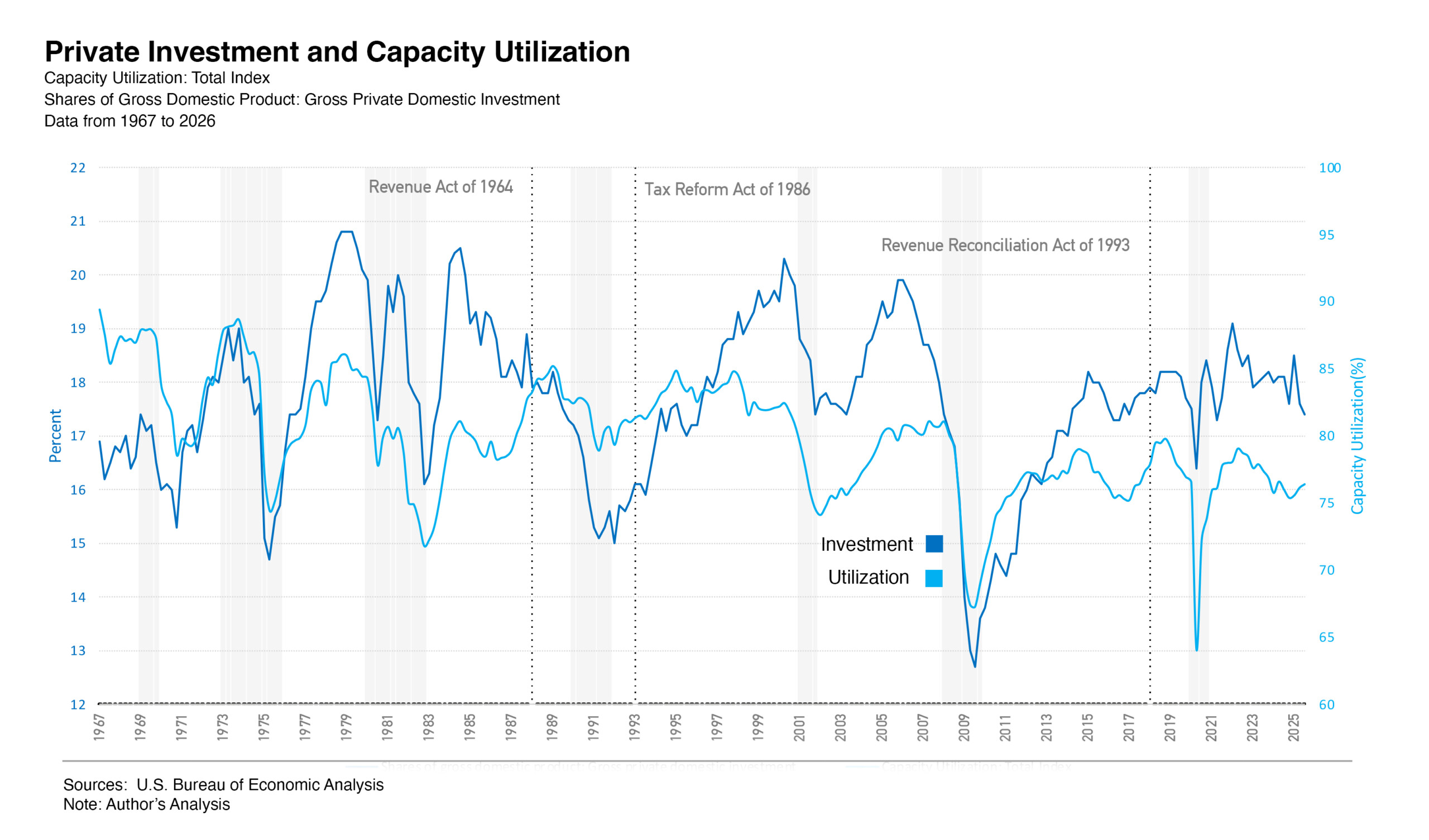

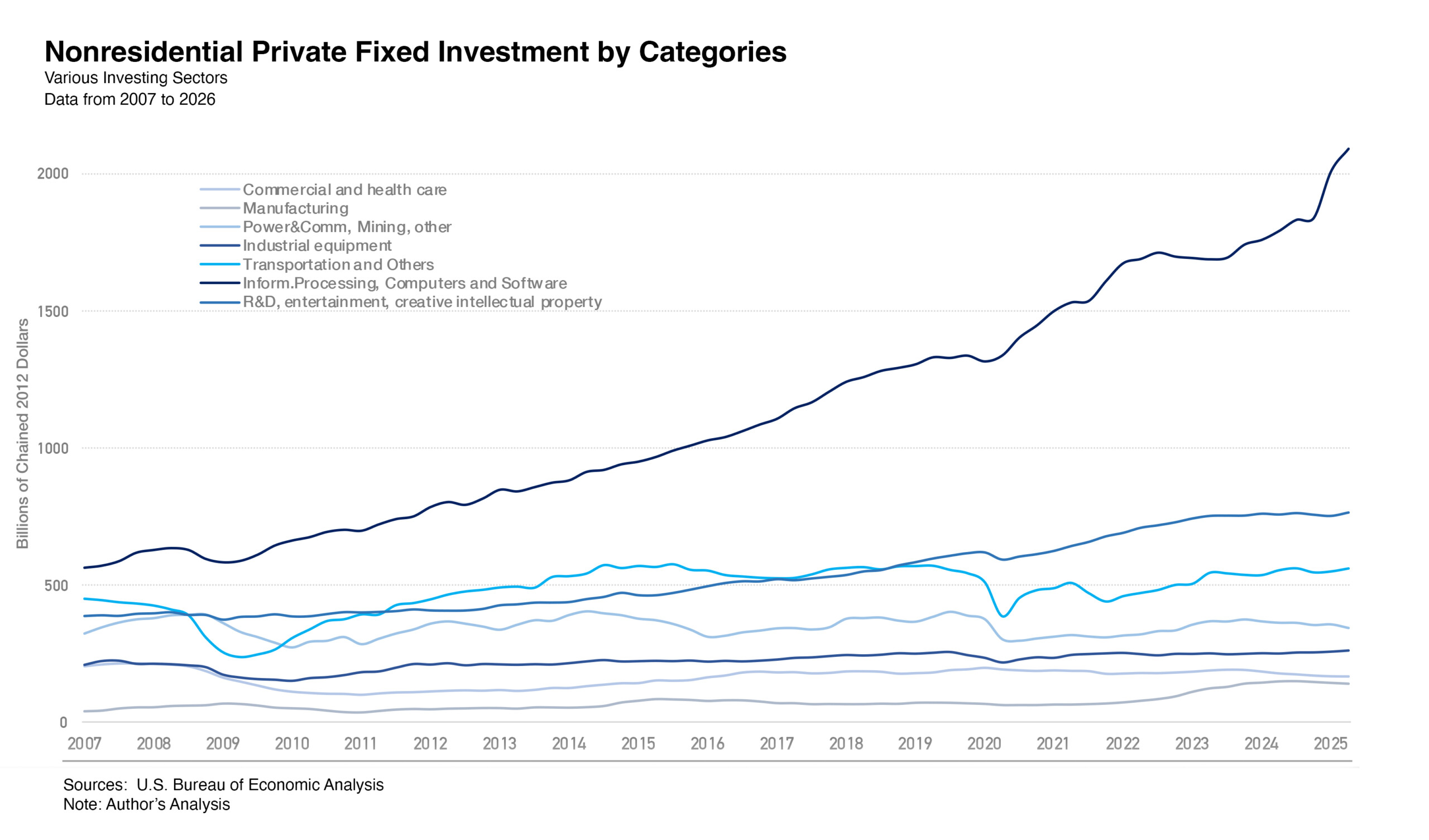

There is a K-shaped growth in consumption expenditures. Most consumption comes from highest income earners. Likewise, there is a K-shaped growth in wages. Since the pandemic, growth in the wages of lowest income groups has fallen below that of all other income categories. Investment remains below it’s pre-2007 recession level and is not correlated with corporate tax breaks or with interest rates, but with capacity utilization. Corporate America’s reluctance to reinvest reflects the fact that firms already possess more capacity (factories, machines, service capability) than they can fully use.

Investment remains below it’s pre-2007 recession level and is not correlated with corporate tax breaks or with interest rates, but with capacity utilization. Corporate America’s reluctance to reinvest reflects the fact that firms already possess more capacity (factories, machines, service capability) than they can fully use.

Research suggests that the disconnect between rising market valuations (high Tobin’s Q) and weak business investment is accounted for by excess capacity (Ikenberry and Grullon, The Journal of Finance, 2025). This helps explain why periodic corporate tax cuts enacted by the administration have generally failed to revive private investment across most industries.A K-shaped recovery across firms shows strong growth in the tech sector but weakness in most other industries.

In terms of monetary policy, there is a inflation-unemployment trade-off. Standard economic benchmark for monetary policy, the Taylor rule, suggest monetary policy is broadly appropriate. The Taylor rule provides a guideline for the federal funds rate based on current inflation and economic growth. After the pandemic, it indicated that monetary policy was too accommodative, prompting the Federal Reserve to raise interest rates. Given current inflation and economic growth, the rule suggests there is little justification for rates cuts at this time, due to relatively low unemployment but sticky inflation.

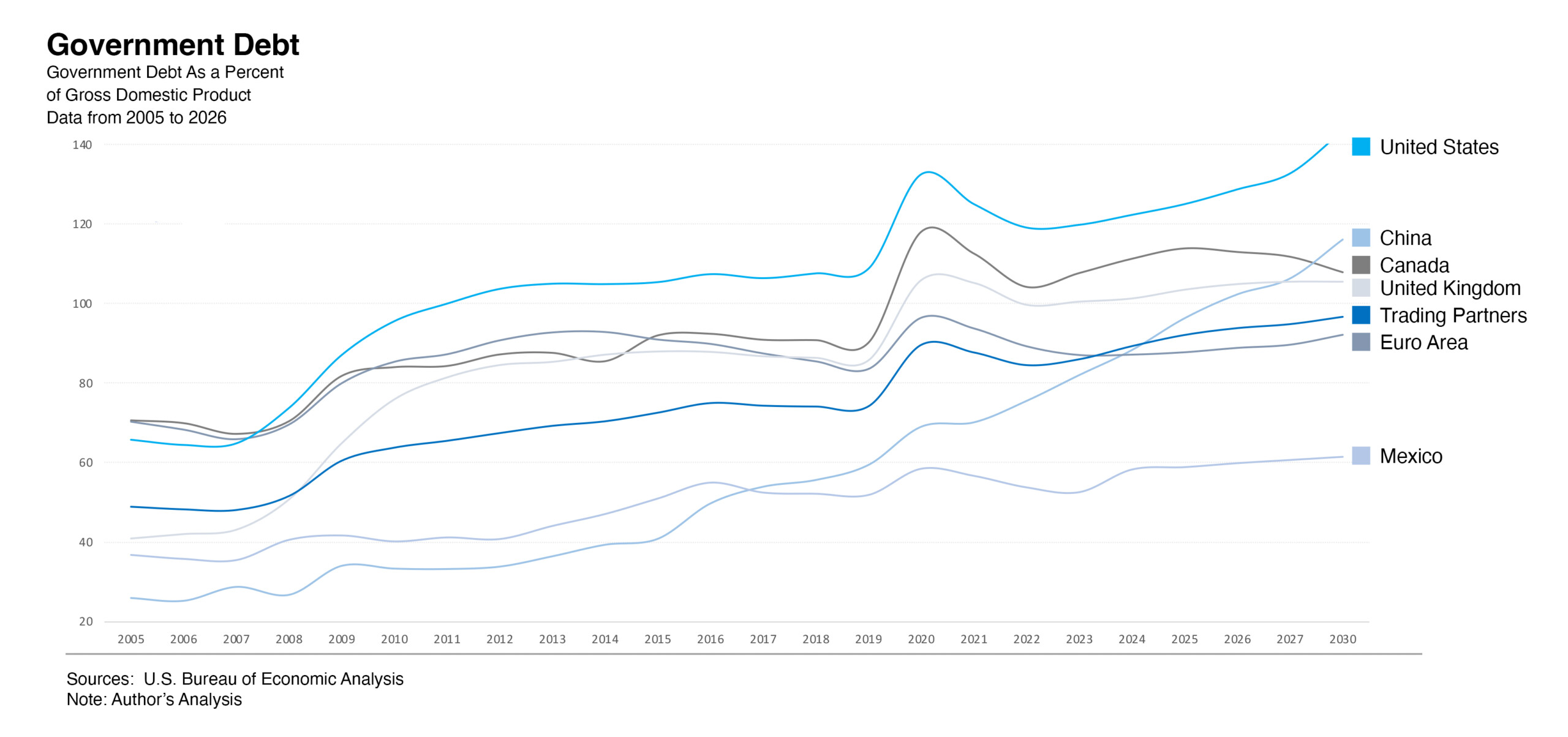

In terms of fiscal policy and government debt, US Government debt was already high before the pandemic, rose sharply thereafter, and is expected to remain elevated relative to peer economies.

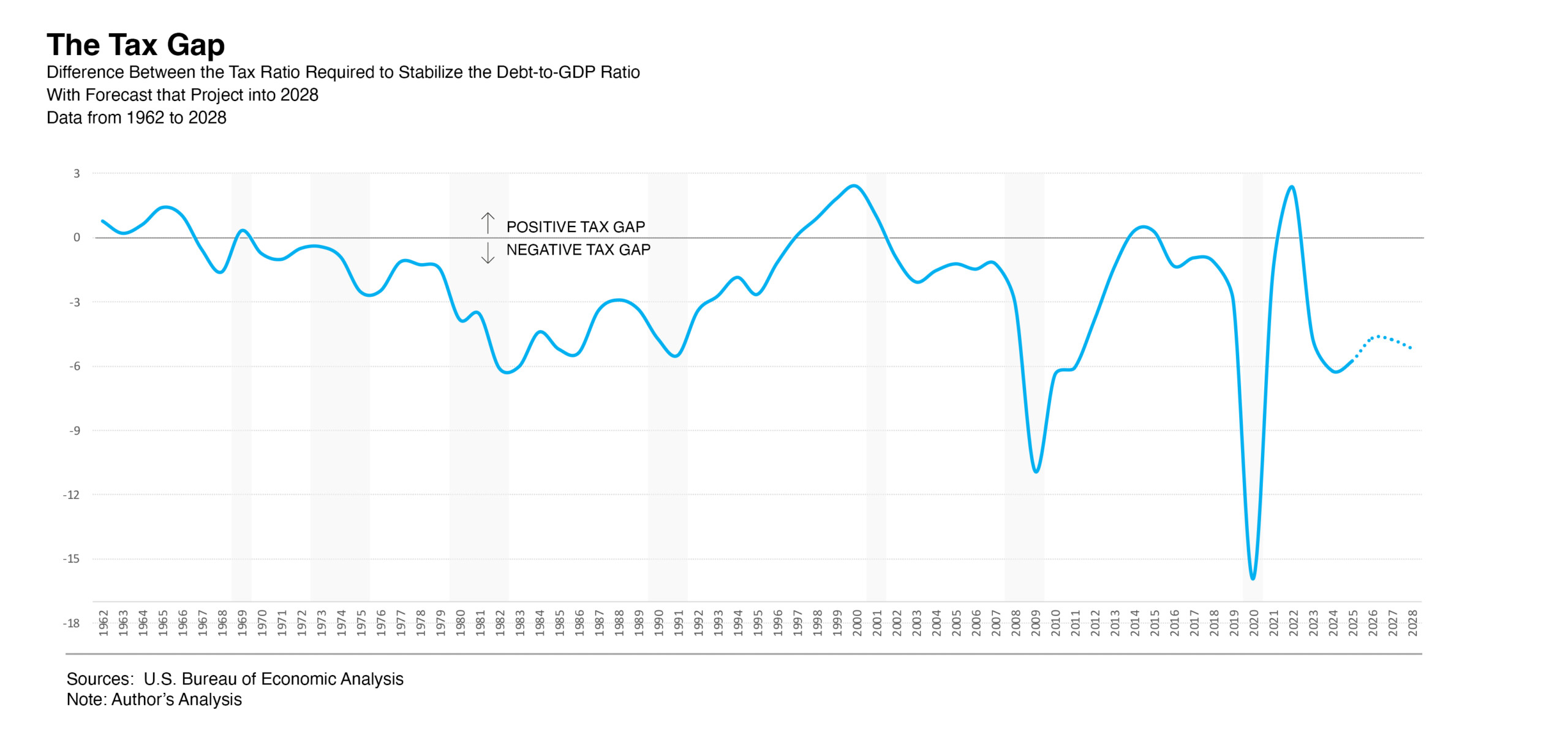

Fiscal policy is unsustainable; the tax gap indicator highlights the need to address the deficit. The tax gap indicator measures the difference between the tax ratio required to stabilize the debt-to-GDP ratio and the current tax ratio consistent with the current inflation and economic growth. A negative value indicates that current taxes are insufficient to stabilize the debt, implying unsustainable fiscal policy. The outlook suggests further deterioration.

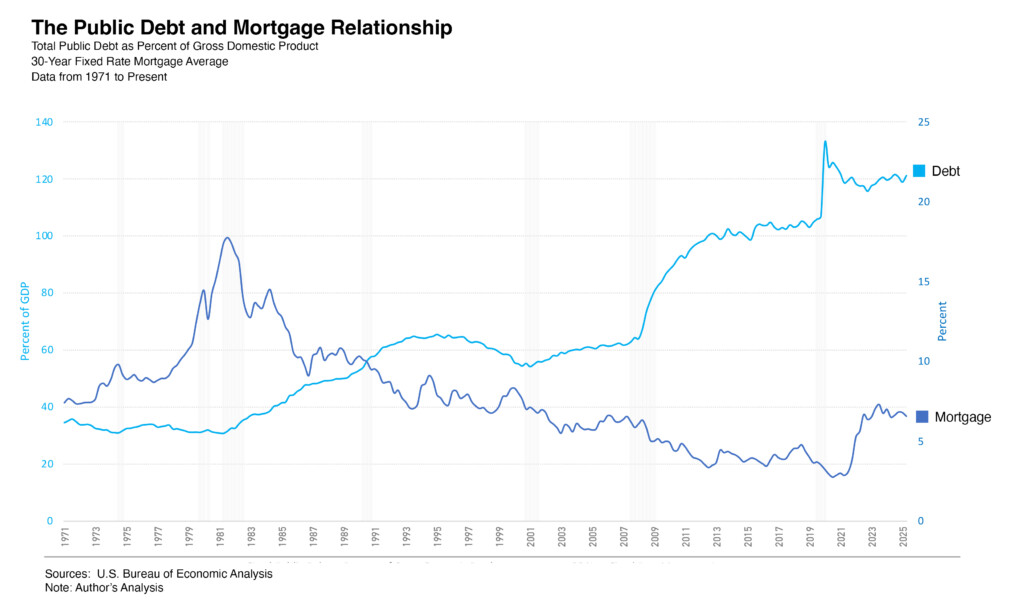

A major concern surrounding high public debt is its potential impact on the housing market through higher long-term interest rates, since mortgage rates are closely tied to the 10-year Treasury yield. And by extension concerns around the relationship between US public debt and mortgage rate.

Strong global demand for US debt has decoupled US public debt from domestic interest rates, limiting the impact on mortgage rates. US public debt shows little correlation with mortgage rates. Empirical studies indicate that increases in public debt significantly raise long-term inflationary expectations in Emerging Market economies but not in advanced economies. In emerging markets, high public debt often forces central banks to combat inflation more aggressively, particularly when inflation is already elevated and central bank credibility is weak.

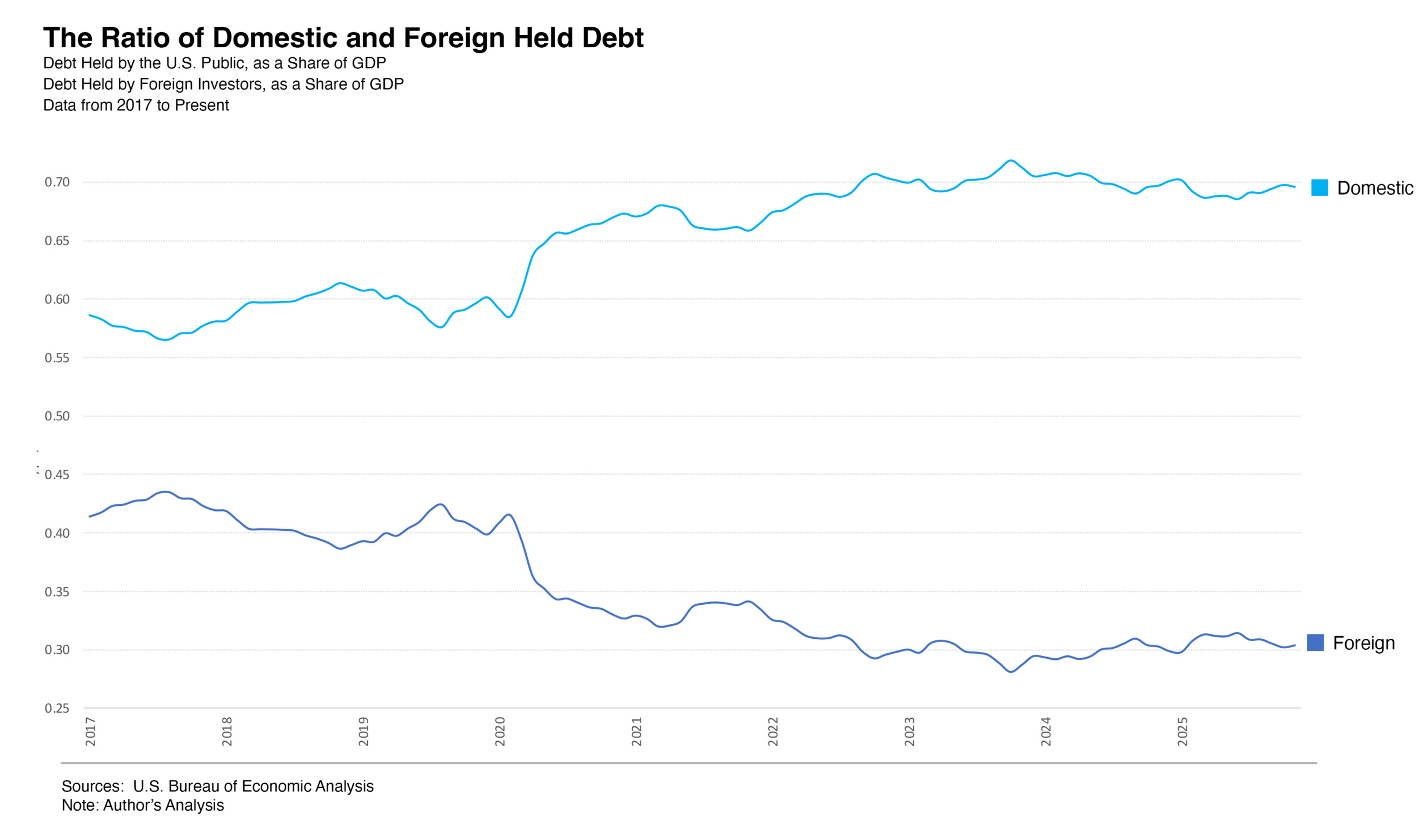

With high deficit and debt the reason the US did not experience crowding-out for the last several decades is largely because foreign investors, have financed a substantial share of US public debt. Despite the geopolitical tensions, the share of US Public debt held by foreign investors has remained relatively stable.

With high deficit and debt the reason the US did not experience crowding-out for the last several decades is largely because foreign investors, have financed a substantial share of US public debt. Despite the geopolitical tensions, the share of US Public debt held by foreign investors has remained relatively stable.

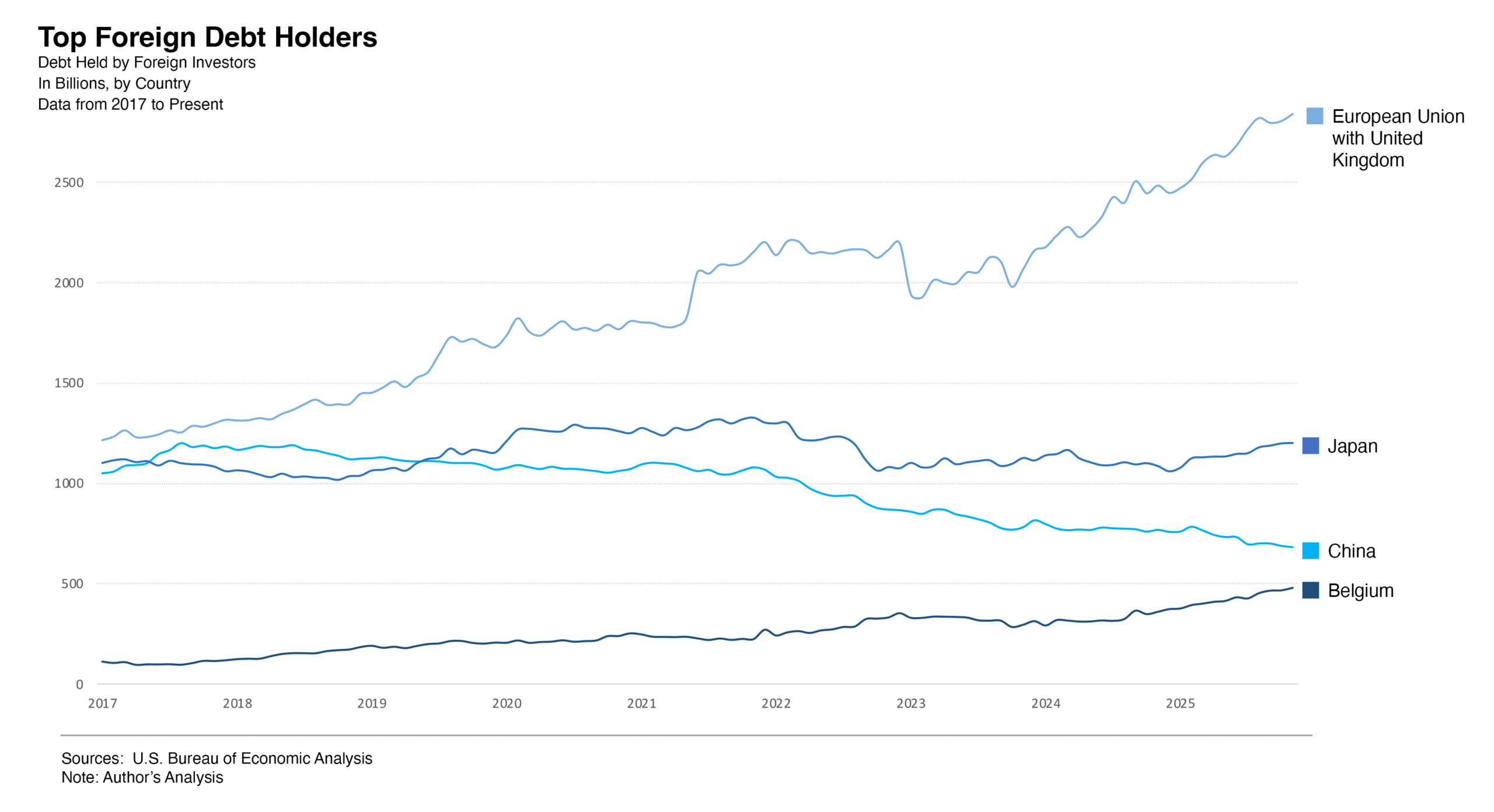

The flight-to-safety dynamics and safe-asset demand are boosting U.S. Treasury buying, with European investors increasing their purchases over the last two years while China has steadily reduced its holdings since 2018.

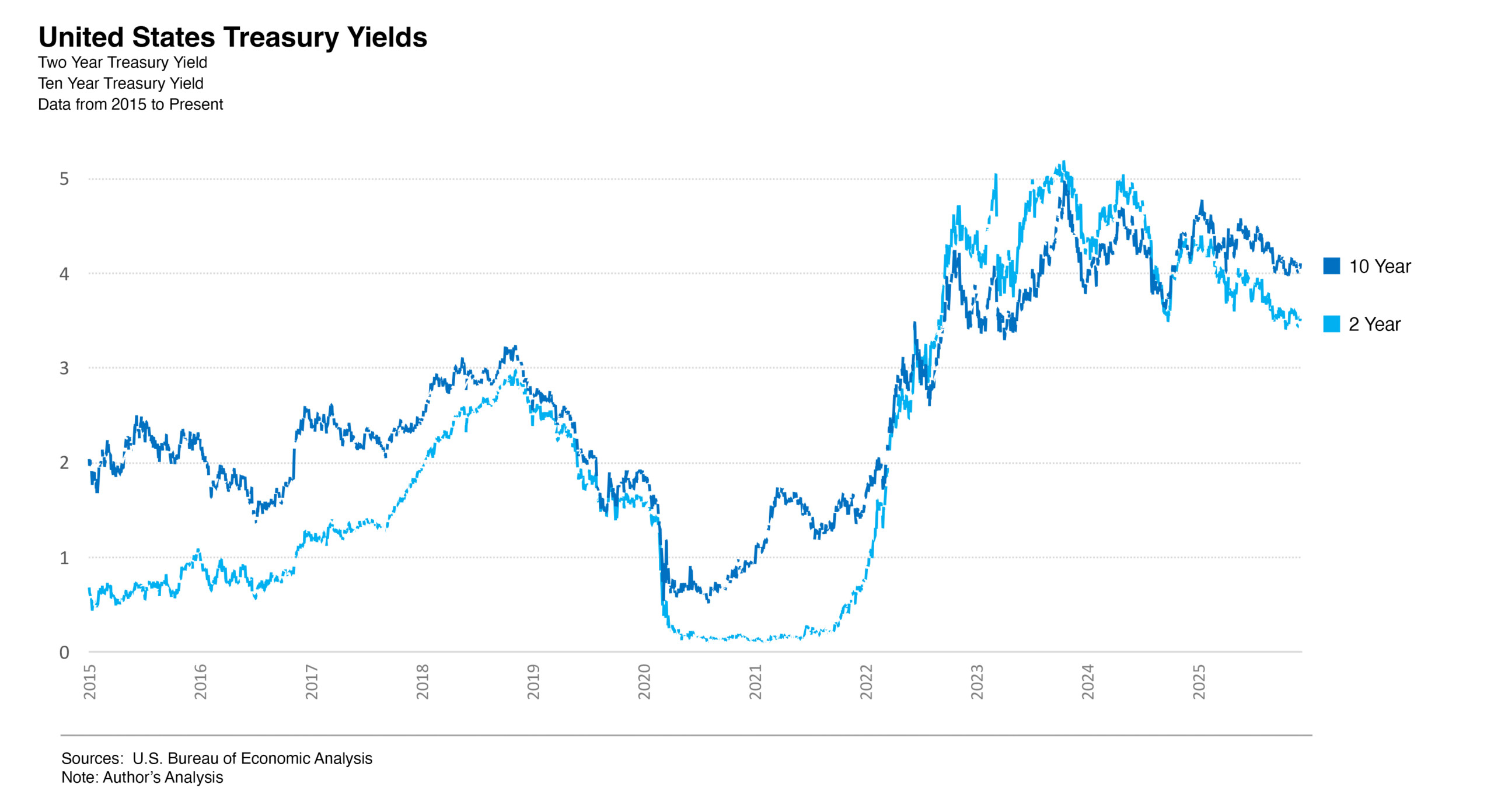

Recession fears at home and abroad are reshaping financial markets and the outlook for U.S. government debt. Investors are pricing in additional Fed cuts, but concerns about a debt crisis are intensifying. Since COVID, a global oversupply of government debt has contributed to higher yields overall. In the United States, rising recession fears have increased expectations of Fed rate cuts, which has pulled down short-term yields such as the 2-year rate. At the same time, worries about fiscal sustainability have kept 10-year yields elevated. Market-implied expectations for the 10-year yield 10 and 20 years ahead continue to trend upward, largely independent of prospective reductions in the federal funds rate. Concerns about public debt are especially acute in the United Kingdom and Germany, and particularly in Japan, where debt-to-GDP is about 240%.

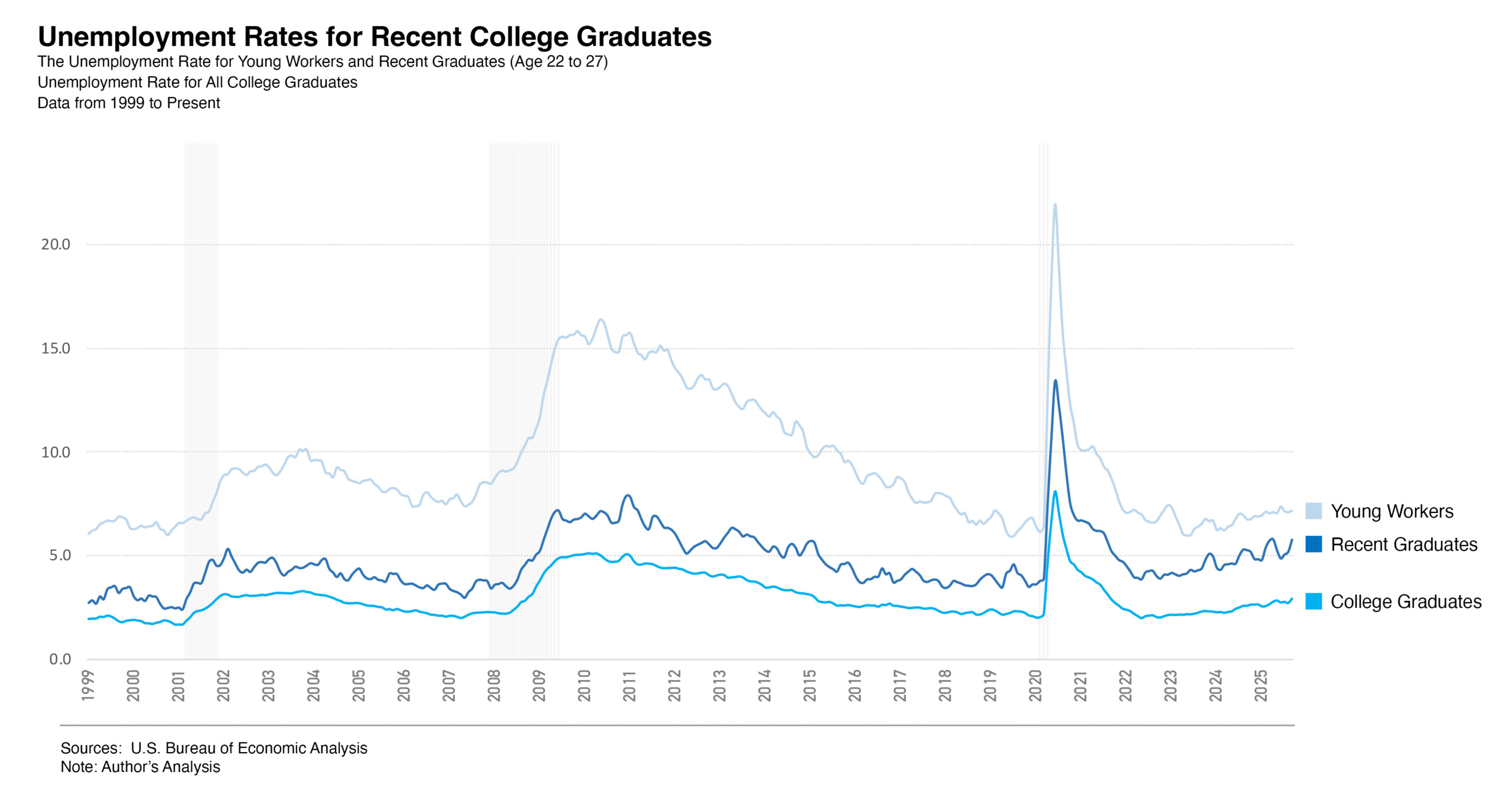

Recent labor market data from the Federal Reserve Bank of New York, the United States Census Bureau, the Bureau of Labor Statistics, and the Current Population Survey point to a “low hiring, low firing” environment, with artificial intelligence playing an increasing role. The evidence also suggests the emergence of “forever layoffs,” meaning recurring rounds of small job cuts that often affect fewer than fifty employees at a time and frequently escape public reporting. At the same time, hiring rates have fallen to their weakest level in ten years. Among young college graduates ages twenty to twenty four, the unemployment rate in the United States has climbed to levels not seen since two thousand fourteen, reaching nine point five percent in September two thousand twenty five, which is almost twice the rate for the overall adult population, and this deterioration predates the coronavirus downturn.

A substantial share of the weakness is concentrated in technology related fields, where unemployment is about seven point five percent for computer engineering graduates and six point one percent for computer science graduates. This aligns with a broader pullback in junior hiring, as firms, especially in the technology industry, have sharply reduced entry level recruitment. Research from Stanford University reports a sixty seven percent decline in United States postings for entry level technology jobs between two thousand twenty three and two thousand twenty four, a shift largely attributed to the spread of artificial intelligence and automation replacing tasks once handled by junior employees, along with employers’ increasing preference for more senior staff.

A potential stock market bubble led by the Tech sector is of concern. The share of the tech sector has risen dramatically over the past decade, up from about 12% in 2015 to 35% today. The concentration of market value in these seven companies has driven much of the S&P 500’s recent performance, while also increasing overall index volatility and the risk associated with a potential bursting of the Tech bubble.

The stock market is increasingly concentrated in the technology sector. The share of the technology sector has risen dramatically over the past decade, up from about twelve percent in two thousand fifteen to thirty five percent today. The concentration of market value in seven companies has driven much of the Standard and Poor’s five hundred’s recent performance, while also increasing overall index volatility and the risk associated with a potential bursting of a technology bubble.

This concentration also resembles a K type bubble, because roughly forty percent of equities are held by top income earners, who also sustain consumption growth. Because consumption is disproportionately supported by top income earners who hold most financial assets, a market crash could significantly reduce aggregate consumption and propagate broader economic weakness. Historically, an additional dollar of stock market wealth is shown to increase consumer spending by up to five cents, so a crash in stock prices can significantly hurt the economy. Even so, current equity valuations remain below the levels observed at the comparable stage of the dot com bubble

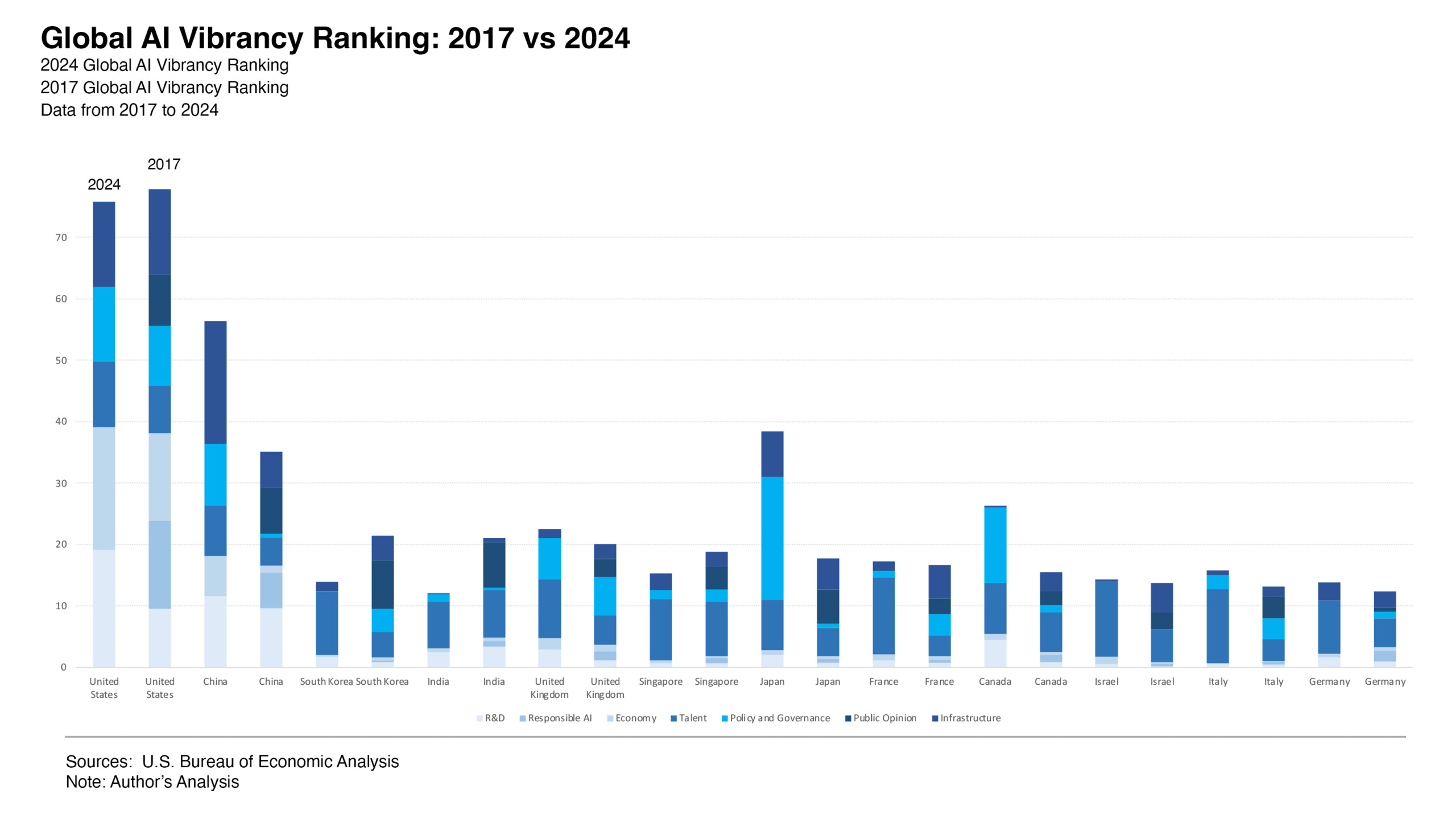

Ground for optimism comes from United States global dominance in artificial intelligence vibrancy. Artificial intelligence vibrancy is an index developed by Stanford University to enable cross country comparison of forty two indicators, including research and development such as academic publications, patents, and machine learning models, responsible artificial intelligence such as conference submissions, economic activity such as private investment in artificial intelligence start ups, artificial intelligence mergers and acquisitions, artificial intelligence hiring, and job postings, public opinion such as social media posts and discussions, and infrastructure such as semiconductor exports, supercomputers, and internet speed.

The United States leads by a wide margin across nearly all categories. Strong investment in artificial intelligence and the broader technology sector reflects market confidence that the United States technological advantage will continue to support economic growth well into the future.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}