Paul Krugman

January 31, 2019

Do you remember the winter of debt?

In late 2010 and early 2011, the U.S. economy had barely begun to recover from the 2008 financial crisis. Around 9 percent of the labor force was still unemployed; long-term unemployment was especially severe, with more than 6 million Americans having been out of work for 6 months or more. You might have expected the continuing employment crisis to be the focus of most economic policy discussion.

But no: Washington was obsessed with debt. The Simpson-Bowles report was the talk of the town. Paul Ryan’s impassioned (and, of course, hypocritical) denunciations of federal debt won him media adulation and awards. And between the capital’s debt obsession, the Republican takeover of the House, and a hard right turn in state governments, America was about to embark on a period of cutbacks in government spending unprecedented in the face of high unemployment.

Some of us protested bitterly against this policy turn, arguing that a period of mass unemployment was no time for fiscal austerity. And we were mostly right. Why only “mostly”? Because it’s becoming increasingly doubtful whether there’s any right time for fiscal austerity. The obsession with debt is looking foolish even at full employment.

That’s the message I take from Olivier Blanchard’s presidential address to the American Economic Association. To be fair, Blanchard — one of the world’s leading macroeconomists, formerly the extremely influential chief economist of the I.M.F. — was cautious in his pronouncements, and certainly didn’t go all MMT and say that debt never matters. But his analysis nonetheless makes the Fix the Debt fixation look even worse than before.

Blanchard starts with the commonplace observation that interest rates on government debt are quite low, which in itself means that worries about debt are overblown. But he makes a more specific point: the average interest rate on debt is less than the economy’s growth rate (“r<g”). Moreover, this isn’t a temporary aberration: interest rates less than growth are actually the norm, broken only for a relatively short stretch in the 1980s.

Why does this matter? There are actually two separate but related implications of low interest rates. First, fears of a runaway spiral of rising debt are based on a myth. Second, raising private investment shouldn’t be a huge priority.

On the first point: Diatribes about debt often come with ominous warnings that debt may snowball over time. That is, high debt will mean high interest payments, which drive up deficits, leading to even more debt, which leads to even higher interest rates, and so on.

But what matters for government solvency isn’t the absolute level of debt but its level relative to the tax base, which in turn basically corresponds to the size of the economy. And the dollar value of G.D.P. normally grows over time, due to both growth and inflation. Other things equal, this gradually melts the snowball: even if debt is rising in dollar terms, it will shrink as a percentage of G.D.P. if deficits aren’t too large.

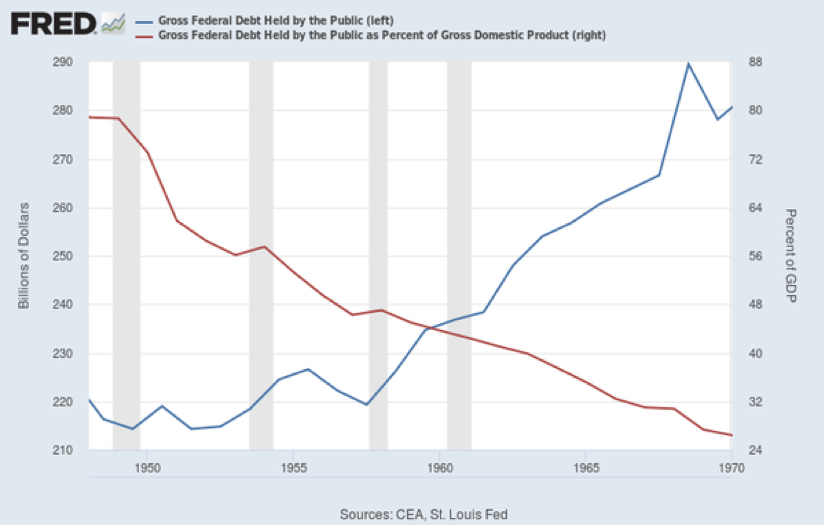

The classic example is what happened to U.S. debt from World War II. When and how did we pay it off? The answer is that we never did. Yet as Figure 1 shows, despite rising dollar debt, by 1970 growth and inflation had reduced the debt to an easily handled share of G.D.P.

Figure 1: Gross Federal Debt vs. Gross Federal Debt Held by the Public as Percent of GDP

And if interest rates are less than G.D.P. growth, this effect means that debt tends to melt away of its own accord: a high debt level means higher interest payments, but it also means more melting, and the latter effect predominates. A self-reinforcing debt spiral just doesn’t happen.

Blanchard’s second point is subtler but still important. In general, debt scolds warn not just about threats to government solvency but about growth. The claim is that high public debt feeds current consumption at the expense of investment for the future. And high debt does indeed probably have that effect when the economy is near full employment (although in 2010-2011 more deficit spending would have led to more, not less, private investment).

But how important is it to suppress consumption to free up resources for investment? What Blanchard points out is that low interest rates are an indication that the private sector sees fairly low returns on investment, so that diverting more resources to private investment won’t make that much difference to growth. True, the rate of return on investment is surely higher than the interest rate on safe assets like U.S. Treasuries. But Blanchard makes the case that it’s not as much higher as many seem to think.

Does this mean that we should eat, drink, be merry, and forget about the future? No — but private investment isn’t the big issue, since it probably doesn’t have a very high rate of return. Blanchard doesn’t say this, but what we should probably be worrying about instead is public investment in infrastructure, which has been neglected and suffers from obvious deficiencies.

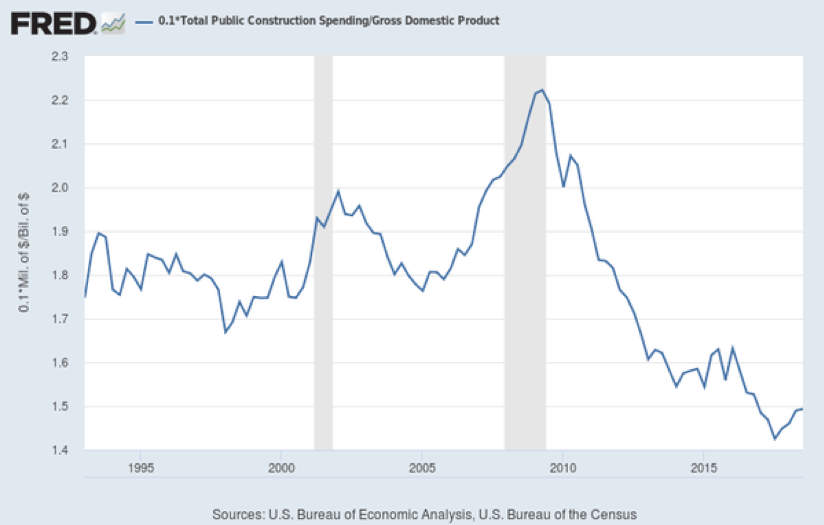

Yet the debt obsession led to less, not more, public investment. Figure 2 shows public construction spending as a percentage of G.D.P. It rose briefly during the Obama stimulus (partly because G.D.P. was down), then plunged to historically low levels, where it has stayed. For all the talk about taking care of future generations, debt scolds have almost surely hurt, not helped, our future prospects.

Figure 2: Total Public Construction Spending as a Share of GDP

Notice that I haven’t even talked about business-cycle-related reasons to stop obsessing over debt. An environment of persistently low interest rates raises concerns about secular stagnation — a tendency to suffer repeated intractable slumps, because the Fed doesn’t have enough ammunition to fight them. And such slumps may reduce long-term growth as well: the experience since 2008 suggests a high degree of hysteresis, in which seemingly short-run downturns end up reducing long-run economic potential.

But even without these concerns, debt looks like a hugely overblown issue, and the way debt displaced unemployment at the heart of public debate in 2010-2011 just keeps looking worse.

This article is adapted from P. Krugman’s January 9, 2019 New York Times Opinion blog.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}